Does the recent

and unprecedented increase in the minority wanting a smaller state

reflect the non-indexation of tax thresholds? If it does, are social attitudes a

problem for those economists arguing to end the zero-rating of many

goods for VAT?

The National Centre

for Social Research produces an annual survey about British Social

Attitudes, and they have issued

a preliminary look at the survey conducted in the

Autumn of last year. One question that I have looked at a number of

times in previous years has concerned attitudes to taxes and public

spending. The latest results are both surprising and imteresting.

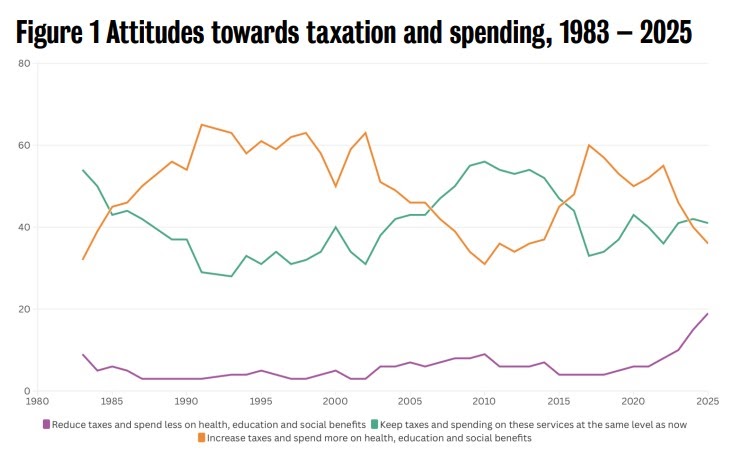

As I have regularly

noted, over the 40+ years of the survey the number of people saying

they wanted lower taxes and spending (a smaller state) has been

remarkably low at less than 10%. Remarkable, that is, given the

prominence that view gets in public discourse. But not any more. In

the last few years this proportion has grown significantly, and is

now at 19%.

Why is this? The

most obvious explanation is that taxes are going up, which is true.

But total taxes have risen before, and we haven’t seen this

response in public attitudes. Here is the share of total taxes in GDP

from the OBR’s database.

Taxes have risen

substantially since the pandemic, but they rose by almost twice as

much from 1993/4 to 2000/1, yet in the social attitudes survey there

is no rise in those wanting a smaller state over that period

comparable with recent movements..

One explanation for

this recent rapid increase in those wanting a smaller state would be

if people were much happier about the level of public services now

compared to the late 1990s. This isn’t plausible because both the

level of public service provision (measured by indicators like

waiting times for hospital appointments) and the level of spending on

public services is

clearly inferior to the period at the end of the last

Labour government, and is at least comparable if not worse than in

the late 1990s. The impact of the austerity period from 2010 onwards

has not been undone.

A more plausible

story is that those answering the survey are not thinking about total

taxes, but rather just taxes on income. Here is a chart from the

Resolution Foundation:

The noteworthy fact

this chart shows is that taxes on income have been falling for most

earners since 1980. [1] This hasn’t been true for the total tax

burden because taxes have been shifting from taxes on income to taxes

on consumption (e.g. VAT) or taxes on profits.

Very few survey

respondents will be aware of the total tax burden they face. What

most will see is the amount of tax taken from their pay each month.

So the recent increase in the number of people wanting a smaller

state could simply reflect the recent rise in the amount of income

tax they are paying, which in turn is mainly the result of the

non-indexation of income tax thresholds, started under the previous

government and continued by Rachel Reeves. [2]

If this

interpretation of the survey is correct (and I’m sure there are

other interpretations) then the main implication for me is that

attitudes to the size of the state depend crucially on the type of

taxes being raised. Public attitudes to the size of the state may

depend on the mix of taxes, with in the longer term the public

accepting higher taxes on consumption and profits more easily than

taxes on income. (In the short term the latter will generate

inflation which is unpopular, but that unpopularity does not seem to

be translated into public attitudes about the size of the state.)

Of course

politicians, particularly on the right, have long suspected this,

which is one reason why there has been a shift away from taxes on

income over the last few decades. To that extent recent public

attitudes are consistent with this belief. Those on the political

left have often favoured higher taxes on income rather than higher

taxes on consumption because the former is thought to be more

progressive. This is true, although VAT in particular is in itself

mildly progressive because there are lower or zero tax rates on

necessities like food, children’s clothing or domestic energy.

However the

progressivity of consumption taxes has been challenged

by economists, who argue there are better, more

effective ways to help poorer people than zero-rating. They, and

journalists, love to tell us about the time wasted on borderline

cases involving Jaffa

cakes and the like, and these compliance costs are

real and waste resources. At least as important is that the better

off also spend large amounts on zero rated items, so zero-rating is a

relatively inefficient way of redistributing income.

In my view a

perfectly legitimate counter argument is that this reasoning neglects

how many people feel about helping the poor in other ways. The same National Centre for Social Research Social Attitudes survey shows more people now disagree than agree that more money should be spent on benefits for the poor. It is fine to argue that the poor can be helped more efficiently by replacing zero-rating with better benefits, but that will not happen if better benefits are impossible to achieve politically, or are gradually reduced in real terms because of public suspicion or even hostility.

To take a more specific example, an economist would argue that benefits (like child benefit)

are better than VAT zero-rating on essentials in part because benefits don’t distort

the choices those receiving them make. But many socially conservative voters might

argue that they are happy to subsidise children’s clothing for the

poor because they know that money is well spent, whereas they will be

more suspicious that money on benefits that the beneficiiary is free to spend as they like will be misspent.

There are many

reasons why people might favour higher taxes and public spending, but

one may simply be that they are unaware of the taxes they pay

indirectly through VAT and elsewhere. This in turn may encourage

politicians to shift the tax burden from direct to indirect taxes.

Economists argue quite rightly that VAT zero-rating on essential

items is an inefficient means of redistribution, but making indirect

taxes more regressive could end up making the overall tax and benefit

system less progressive if socially conservative voters and the

politicians that represent them squeeze benefits.

[1] The only

exception is for high earners, but they are likely to make up a good

proportion of those who always thought that their taxes should be

lower.

[2] An interesting

question is whether the impact of the non-indexation of thresholds

has been more noticeable ex post by survey respondents than the same

amount of revenue raised by raising tax rates would have been,

because it has meant that some are now paying income tax for the

first time.

Source link